However, when determining whether they have enough evidence on file the auditor must consider:

- the risk of material misstatement;

- the materiality of the item;

- the nature of accounting and internal control systems;

- the auditor’s knowledge and experience of the business;

- the results of controls tests;

What constitutes sufficient appropriate audit evidence is a matter of judgment?

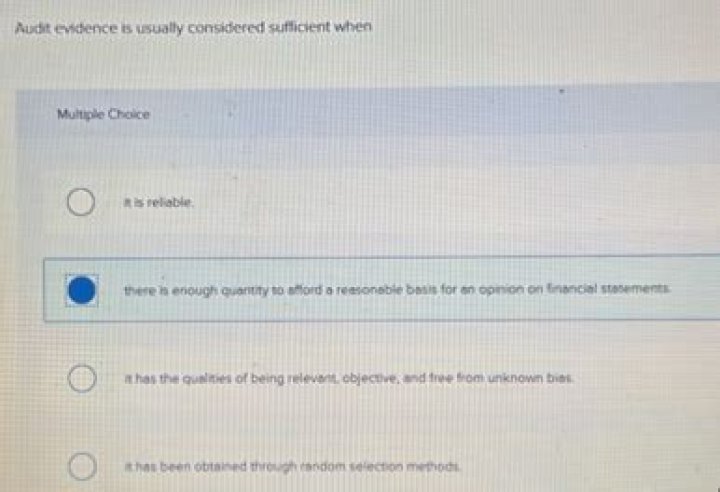

Sufficiency is the measure of the quantity of audit evidence. … Whether the audit evidence obtained in the course of an engagement is sufficient and appropriate to support the auditor’s opinion is a matter of professional judgment that the auditor needs to establish.

What is appropriate and sufficient evidence?

Sufficiency is the measure of the quantity of audit evidence. … Appropriateness is the measure of the quality of audit evidence; that is, its relevance and its reliability in providing support for the conclusions on which the auditor’s opinion is based.

What should the auditor do if the auditor can’t obtain sufficient appropriate audit evidence?

If the auditor is unable to obtain sufficient appropriate audit evidence, the auditor shall express a qualified opinion or disclaim an opinion on the financial statements.

Why does the auditor need evidence?

Audit evidence is evidence obtained by auditors during a financial audit and recorded in the audit working papers. Auditors need audit evidence to see if a company has the correct information considering their financial transactions so a C.P.A. (Certified Public Accountant) can confirm their financial statements.

What is audit evidence and documentation?

Audit evidence refers to Information used by the auditor in arriving at the conclusions on which the auditor’s opinion is based. … Among other things, audit documentation includes records of the planning and performance of the work, the procedures performed, evidence obtained, and conclusions reached by the auditor.

What is the importance of gathering and documenting evidence to the audit?

Audit evidence is important because it is all the information that an auditor gathers to reach his audit opinion about an organization’s financial statements and/or internal control environment.

Which of the following is most reliable source of audit evidence?

Audit evidence is more reliable when it exists in documentary form, whether paper, electronic, or other medium (for example, a contempo- raneously written record of a meeting is more reliable than a subse- quent oral representation of the matters discussed). audit evidence provided by photocopies or facsimiles.

Are the accounting records sufficient audit evidence?

The entries in the accounting records are often initiated, recorded, processed and reported in electronic form. … However, because accounting records alone do not provide sufficient audit evidence on which to base an audit opinion on the financial statements, the auditor obtains other audit evidence.

Which statement is correct regarding the sufficiency and appropriateness of audit evidence?

Which statement is correct regarding the sufficiency and appropriateness of audit evidence? a. Sufficiency is the measure of the quality of audit evidence. transactions, account balances, and disclosures and related assertions.

What is audit evidence and types?

The auditor can obtain different types of audit evidence, and it includes Physical Examination, documentation, analytical procedure, observations, confirmations, inquiries, etc. The type and amount are dependent on the type of organization that is being audited and the required audit scope.What is primary audit evidence?

Primary sources of audit evidence involve the following: Elemental documentation of the company and the accounting system. Tangible assets. Personnel and the administration of the company. Suppliers, customers, knowledge of the company’s business and other parties dealing with the company.

What are the sources of audit evidence?

5 common sources of substantive audit evidence

- Confirmation letters. Auditors send letters to third parties, such as customers or vendors, asking them to verify amounts recorded in the company’s books. …

- Original source documents. …

- Physical observations. …

- Comparisons to external market data. …

- Recalculations.

What are the factors that may influence the auditors Judgement on the sufficiency and appropriateness audit evidence?

The auditor’s judgment as to what is sufficient appropriate audit evidence is influence by such factors: Auditor’s assessment of the nature and the level of inherent risk at the both FS level and the account balance or class of transactions level.

What determines the amount and quality of audit evidence that is needed to complete an audit?

You determine the amount of audit evidence you need by considering the risk of material misstatement and the overall quality of the evidence you receive. … Persuasive evidence tips the scale one way or the other and provides you with a basis beyond a reasonable doubt for forming an opinion.

What are the factors that influence the reliability of audit evidence?

Factors that highly affect the reliability of audit evidence are:

- Source ; Source is evaluated based on its provider’s independence, objectivity, internal control’s strength and etc.

- Verifiability ; Such as Official Receipts with OR number, Particulars, date and company name and etc.